Errors in credit reports are quite common. In fact, it is estimated that one in four credit reports has some type of errors. The wrong information on your report can act as red flags, which can lead to your loan application being rejected.

So, what should you do? Here’s a short guide on the common credit report errors and the ways to resolve them.

The possible errors

Personal information errors: There have been instances where credit bureaus confuse one consumer with another. This primarily happens because of errors in personal information. Thus, check your details, such as name, address, contact details, PAN details, date of birth, etc. diligently.

Accounts errors: There could be errors in the actual status of your accounts, too. Such errors can significantly cut back your credit score. Some of the common errors that you must look out for include:

- An opened account is reported closed, or vice versa

- Timely account payments are reported late or delinquent

- Incorrect dates of late payments

- Incorrect current balance or credit limit

- Unknown accounts or transactions in your name

Mistaken accounts: There are situations when accounts get mistaken. This often happens when another consumer has the same name as yours. This could also be because of identity theft.

Your next step

If you notice an error in one of your reports, then it is advisable to check reports from all credit bureaus. In 2017, the Reserve Bank of India (RBI) made it mandatory for all credit information bureaus in the country to provide a full credit report, on-demand and without any charge, to individuals whose credit history is available with them. Since you can avail one free report from each bureau, this means that you can get four free reports every year.

At present, there are four such companies in India. These are:

- CRIF High Mark Credit Information Services Pvt. Ltd

- Equifax Credit Information Services Pvt. Ltd

- Experian Credit Information Co. of India Pvt. Ltd

- Transunion Cibil Ltd.

If all your reports have errors, it could be the mistake at your lender’s end. But if only one of the reports has errors, then it could be an issue at the credit bureau’s end.

How to resolve the errors?

- Raise a dispute with the bureau and your lender: The simplest way to resolve errors in your credit report is by downloading the dispute form from the respective credit bureau’s website and notifying them. Simultaneously, also write and speak to your lender. Make sure to submit relevant proof of details to make your case stronger.

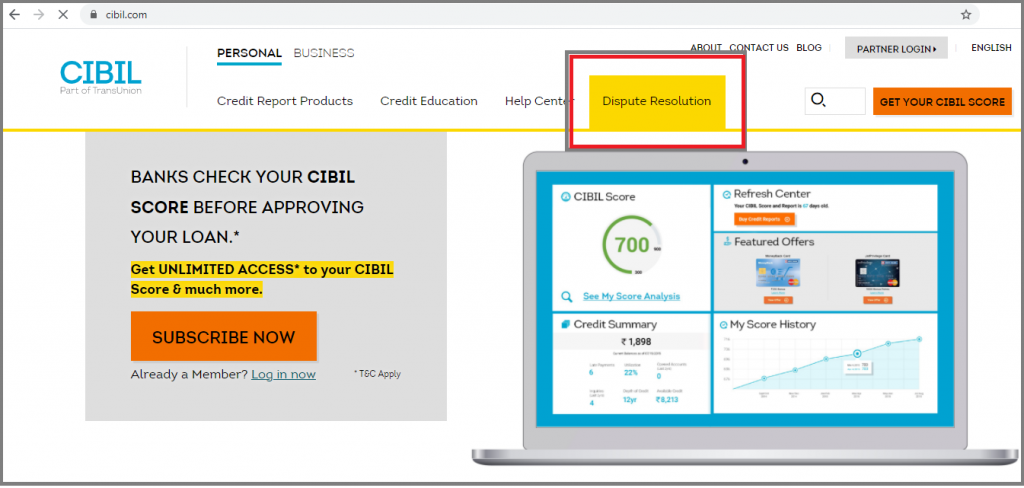

- Raise a complaint with CIBIL: You can also visit the Dispute Resolution section on the CIBIL website and fill out a complaint form. For this, you need the nine-digit number provided on your credit report that contains the disputed details.

In case your issue does not get resolved, here are your options:

- Reach out to the banking ombudsman: If your lender is unable to help you, write to the banking ombudsman. The ombudsman takes it up with the lender, and the issue generally gets sorted within 30 days of filing the complaint.

- Consumer court: This should be your last resort. When none of the above measures works, you can always reach out to the consumer court.

Timelines

Once you submit the dispute form, the credit bureau will verify the dispute by approaching the bank. The bank will accept or reject the dispute. Accepted changes will reflect on your credit report.

This entire process usually takes about four to five weeks.