After months of research, Anitha Nair and her husband finally zeroed on a property.

Without much delay, Anitha applied for a home loan only to know that her application was rejected.

The reason, surprisingly, was her low credit score!

So, if you’ve found your dream home and are opting for a home loan, here are a few things you need to keep in mind about the credit score.

The basics

Before anything else is taken into consideration, the bank will do a thorough check of your income level, your current expenses, and the credit information report from the Central Information Bureau India Limited (CIBIL).

CIBIL is a company that keeps track of an individual’s finances pertaining to credit cards and loans. Banks and other lenders send information reports to CIBIL every month. Using this information, CIBIL creates a Credit Information Report (CIR) and provides a credit score for an individual.

How is credit score calculated?

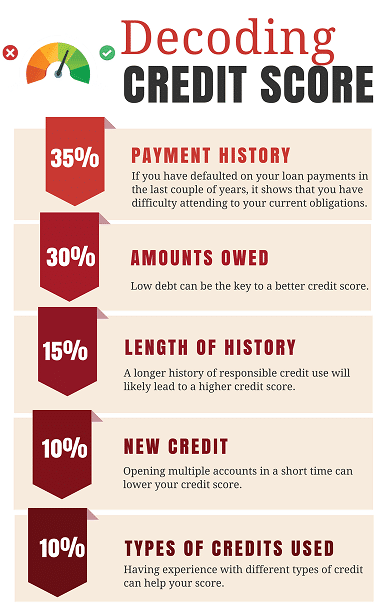

Your credit score calculations depend on various factors. However, three of the most important ones are:

Your credit score calculations depend on various factors. However, three of the most important ones are:

- Last three years calculation of your loan EMIs and bills

- Credit card limit usage

- Percentage of secured and unsecured loan

Naturally, it is important for you to know what factors play a part in achieving a great credit score – the key to obtaining a home loan. Ask yourself the following questions before you apply for a loan:

Question 1: Have I defaulted payments on any existing loans over the last couple of years?

If you have defaulted on your loan payments in the last couple of years, it shows that you have difficulty attending to your current obligations.

Question 2: Is my current balance on the credit card too high?

Using too much credit will likely influence your score negatively as it indicates a higher repayment burden.

Question 3: Have I been “credit hungry”?

If you’ve been applying for one too many loans and/or have been recently sanctioned new credit facilities, it shows increased debt burden, which in turn is likely to negatively impact your score.

If the answer to all the three questions is NO, the chances of your home loan getting sanctioned is very high. In case, the answer is YES to all the questions, then you might have to rework and stabilise your financial situation.

How can I check my credit score for free?

In 2017, the Reserve Bank of India (RBI) made it mandatory for all credit information bureaus in the country to provide a full credit report, on demand and without any charge, to individuals whose credit history is available with them.

At present, there are four such companies in India. These are:

- CRIF High Mark Credit Information Services Pvt. Ltd

- Equifax Credit Information Services Pvt. Ltd

- Experian Credit Information Co. of India Pvt. Ltd

- Transunion Cibil Ltd.

Since you can avail one free report from each bureau, this means that you can get four free reports every year.

Step 1: Begin with the big four credit bureaus. While there are several portals that provide your credit report for free, it is advisable to go for the credit bureaus at first. You can select any one of the four mentioned above.

In this article, we have used CRIF India, which is one of India’s leading providers of Credit Information.

Step 2: Log on to https://www.crifhighmark.com/

Step 3: Click on FREE Credit Score.

Step 4: Fill in your details, identification proofs, and address. You have the option of making a payment to receive an instant report or continue with the free report, which is mailed to your e-mail ID within 3-7 working days.

Step 5: Review your report carefully.

Step 6: Authenticate your enquiry.

How do I know if my score is good enough?

All credit bureaus in India assign a score in the range of 300 to 900. Thus, the closer you are to 900, the better the chances of your home loan application getting approved. However, anything above 750 is considered a good credit score.

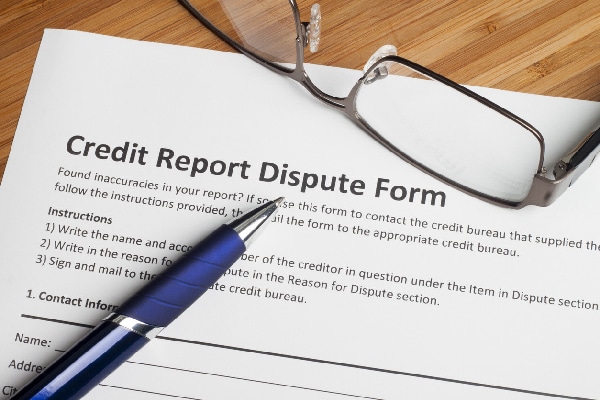

My credit score is low! Could it be wrong?

Yes. Credit reports can have errors, thus reviewing it is imperative. While checking your report, carefully assess the following details.

- Incorrect first and last names

- Addresses of places where you did not live

- Names of employers you did not work for

Also, review each account listed on your credit report. Look out for information that you don’t relate to. For instance:

- Bank accounts you don’t recognise

- Accounts that have been closed but are listed as still open

- Incorrect current balance

- Incorrect account information such as late payments or missed payments

You can correct the information by filling up a dispute resolution form. Here are the steps:

You can correct the information by filling up a dispute resolution form. Here are the steps:

Step 1: Completion and submission of the dispute resolution form to the credit bureau

Step 2: The credit bureau takes up the dispute with the concerned lender

Step 3: The lender accepts or rejects the dispute

Step 4: Accepted changes are reflected on your credit report

This entire process usually takes about four to five weeks.

Can I buy a home with a bad score?

Well, if your score is below 650, you can opt for NBFCs rather than banks. A few of the NBFCs even accept collaterals such as large premiums or gold jewellery. However, these loans will always come at a higher interest rate.

Another way out is to assure the bank by introducing a reliable guarantor. In such a case, the guarantor must have robust finances and a good credit score.

However, we suggest that you work on improving your score before applying for a loan.

If you have any further queries, feel free to drop us a comment below.