National Director

Head of Operations – Strategic Consulting

JLL, India

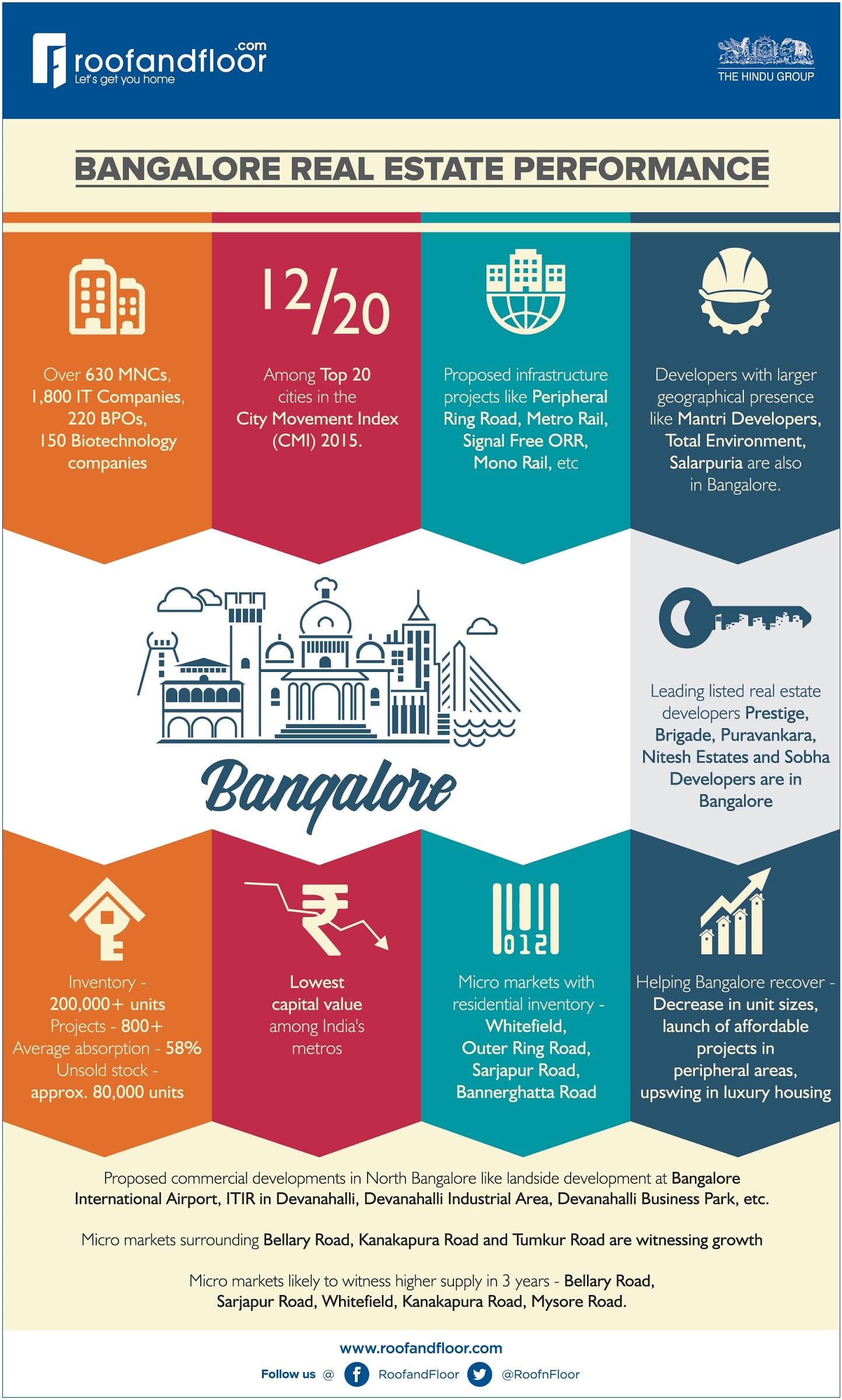

Being the fifth largest city in India with a total population of more than 9 million, Bangalore is one of the preferred investment destinations in India. The largest concentration of IT and ITES-BPO companies – over 630 MNCs, 1,800 IT companies, 220 BPOs and 150 Biotechnology companies – makes Bangalore the largest software exporter and IT hub of India. Bangalore provides India’s first appearance (ranked 12th) among Top 20 cities in the City Movement Index (CMI) 2015. The tremendous growth of the IT / ITES industry has revolutionized the residential real estate and retail markets, and triggered massive infrastructure development. The leisure and entertainment options for the city are abundant. The availability of high quality, large office spaces at sub-dollar rental levels (providing lower operational costs), access to a large skilled workforce, the growth of the retail and residential markets and Bangalore’s cosmopolitan culture have worked in the city’s favour, making it a preferred destination.

Growth in the IT Industry and a rapidly increasing number of High Net-Worth Individuals, and movement of expatriates are the driving force behind Bangalore’s real estate market. The proposed infrastructure projects such as Peripheral Ring Road, Metro Rail, Signal Free ORR, Mono Rail, etc and the proposed commercial developments in North Bangalore such as landside development at Bangalore International Airport, ITIR in Devanahalli, Devanahalli Industrial Area, Devanahalli Business Park, etc will further attract more demand for real estate. The recent Invest Karnataka Summit 2016 attracted funds for the aerospace, biotech and information technology industries, as well as for the development of the state’s infrastructure which would boost the overall city development with generation of more employment.

Bangalore City is home for some of the leading listed real estate developers of the country like Prestige, Brigade, Puravankara, Nitesh Estates and Sobha Developers. This apart, Bangalore also has developers, who have larger geographical presence like Mantri Developers, Total Environment, Salarpuria, etc.

Rushing Residential Sector

The residential sector is witnessed to be one of the strong and competitive markets in Bangalore. At present, the inventory witnessed to be 200,000+ units from 800+ projects with an average absorption of 58%. The unsold stock is witnessed to be approximately 80,000 units. However, Bangalore market witnessed to have the lowest capital value compared to other metro cities, which has improved the buyers’ sentiment resulting in good absorption of residential units in few micro markets of Bangalore. The decrease in unit sizes, launch of affordable projects in peripheral areas will encourage buyer’s sentiment and will match affordability. On the other hand, luxury housing with ticket size upwards of Rs 5 crore is emerging over the last few years for the NRI, HNI and senior management level buyers.

The micro markets such as Whitefield, Outer Ring Road, Sarjapur Road and Bannerghatta Road have significant residential inventory. And micro-markets surrounding Bellary Road, Kanakapura Road and Tumkur Road are witnessing growth in inventory in the recent past. Bangalore City offers inventories in the price band of Rs 4,000-6,000 per sq. ft. in peripheral locations while capital values increase significantly within Central and Secondary Business District where the values start from Rs 7,000 per sq. ft. Reasonable capital values along strong knowledge based economic drivers supported by large infrastructure projects like Metro Rail, Peripheral Ring Road, ORR, etc. are contributing to the growing demand. Bangalore remains an end-user driven market unlike Mumbai and NCR, which have traditionally been speculative, investor-driven markets. This unique characteristic of being an end-user stable market of Bangalore offers an opportunity for investors to hedge a portion of their portfolio for lower down-side risk.

Some of the micro-markets, which are likely to witness higher future supply over next three years include Bellary Road, Sarjapur Road, Whitefield, Kanakapura Road and Mysore Road.

Concentrated Commercial Sector

Bangalore has an inventory of over 96 million sq. ft. of commercial / office space till 1Q2016, which is the second highest supply in the country after Mumbai. Overall, the city’s commercial vacancy stands at 4%, which is the lowest ever vacancy recorded by any of the metro cities. The city saw the highest leasing volumes on the back of big-ticket transactions with a size more than 2 million square feet in Asia Pacific during 1Q2016. The average lease rental is recorded to be Rs 59 per sq.ft per month.

The office space is highly concentrated in Secondary Business District (SBD) with a share of 58% followed by Whitefield with 27% share of the total city stock. The highest absorption is witnessed in SBD during 1Q2016. Large future supply of approx. 10 million sq. ft is expected in SBD micro market in the next three years. SBD commands an average rental rate of Rs 69 per sq. ft whereas the other suburban locations such as Whitefield and Electronic City command rental rate in the range of Rs 28-37 per sq.ft. Sarjapur ORR and Bellary Road are also emerging as office destinations. These locations are preferred by companies primarily due to the presence of good infrastructure and residential micro-markets in the vicinity. The city’s successful corporate space has been primarily driven by the nominal rental rates, availability of quality space, political stability over the years, the country’s largest expatriate population, and availability of top talent for business, high quality living and other advantages. A supply growth of 15% is expected in next three years mainly from SBD and Whitefield.

Developers like Embassy Group, RMZ Corp, Prestige Group and Bagmane are some of the developers holding very high commercial / office inventory in their books and Embassy and RMZ Corp. are one of the top 3 developers in India in terms of stock. Both Embassy and RMZ Corp. have the backing of private equity companies like Blackstone and Qatar Investments, who are ensuring smooth cash flow for portfolio development. Both Embassy and RMZ Corp. are likely to go for listing under REIT in near future.