Haven’t we all received umpteen calls from various banks offering an instant home loan? Well, this is the story of almost every salaried individual as your constant income (read salary) is a testimony to your loan repayment capacity in the bank’s eyes.

However, for self-employed or non-salaried individuals, it is not the same. Having said that, it’s not true that non-salaried individuals cannot avail a home loan. While the process might be smoother for salaried individuals, a non-salaried person can also get a home loan easily, provided they have all the documents in place.

In this post, let us help you with the procedure to get a home loan for non-salaried individuals the RoofandFloor way – simple and hassle-free.

The key factors

There are certain factors that can increase your chances of getting a home loan. These include:

Your repayment capacity

- Age

- Stable income source

- Your liabilities

- Assets

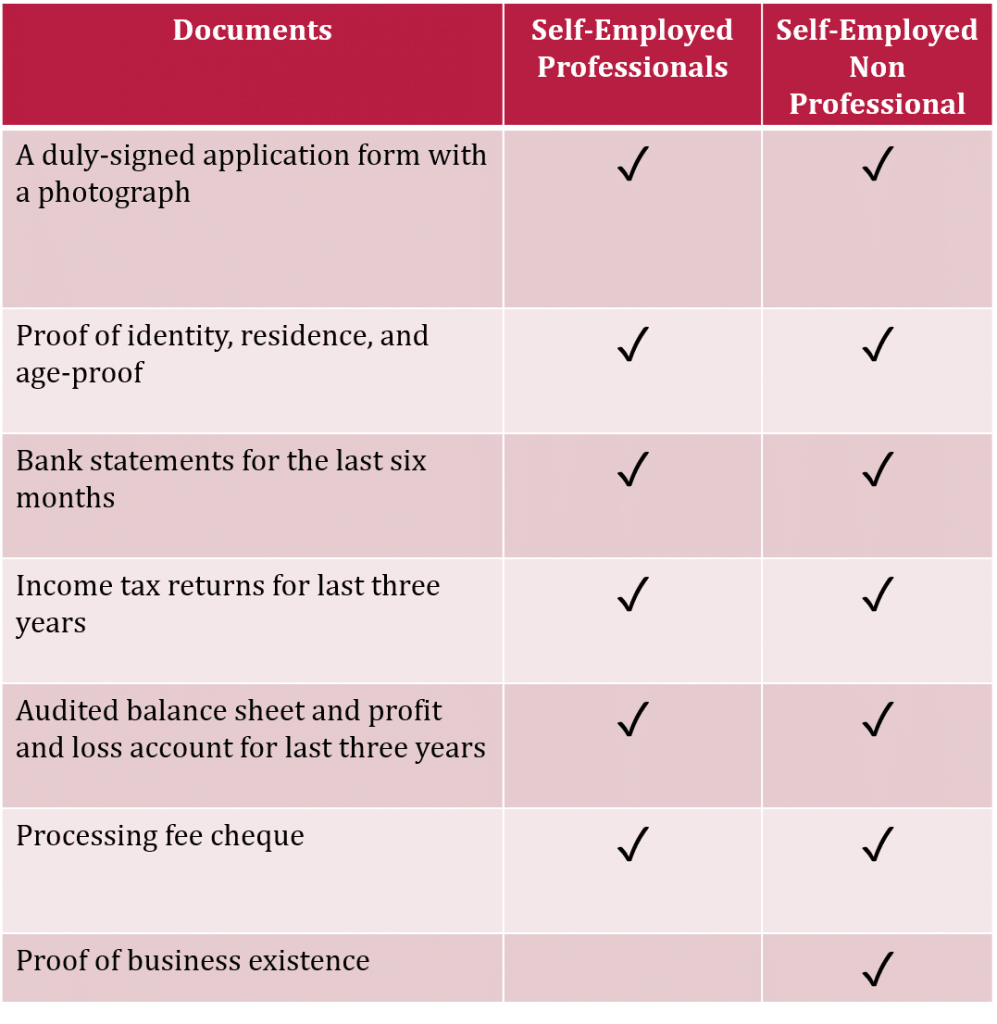

The documentation

Now, let’s move to the paperwork.

Like salaried individuals, all applicants must provide documentation involving KYC (know your customer) norms.

Next in line is some alternative documents to Form 16. This could be a single document submitted to the IT department stating:

- All sources of income

- Income tax return for the last three years

- Audited profit and loss account

- Balance sheet approved by a certified chartered accountant

- Repayment track of running loans

For shopkeepers and traders, producing the shop establishment licence is mandatory.

Once your documentation is sorted, you will have a personal discussion with the bank personnel. In this meeting, the bank will try to understand your business model, the risks involved, and the business practices to ascertain your business’ potential.

For qualified professionals

If you are a qualified professional, your chances of getting a home loan are better as you are easily employable.

Banks will check your client list to get information on your income source, income tax return of the last three years, and credit history if any. Along with these documents, you will have to submit the practice certificate and registration certificate for deduction of professional tax.

Owner of proprietary concern

In this case, you must have your registration certificate under the Shop and Establishment Act and Factories Act along with the tax return statement and income statement. You will also have to submit some additional documents like balance sheets. (Refer to the documents mentioned above)

Partner in a firm

If you are in a partnership firm, you must have an updated deed of partnership and identify proof of your partners along with all other above-mentioned documents.

The age factor

A non-salaried person must be 22-65 years of age to avail a home loan. Some banks lend to people up to 70 years, if the succession plan and income proof are available.

The income norm

To secure a home loan as a non-salaried individual, you must have spent at least three years in your business. That’s not all! You will also have to show a minimum cash profit of Rs 1.20 Lakh in the past two-year period.

Loan tenure

The highest loan tenure for non-salaried individuals is 20 years. However, several banks restrict this to 15 years. Check this before finalising a lender.

The loan-to-value rate

The loan-to-value (LTV) ratio varies between 75-80%.

Your banking habits

Having a good credit score really helps in availing a home loan. Additionally, it is advisable that you apply for a home loan from the bank where you maintain your current accounts. This gives the bank a clear picture of your cash flows and spends.

In a nutshell, all you have to do is to have your documents in order, and you will be sorted. Still got doubts? Do let us know in the comments below.