Despite high demand, the new supply of residential properties dropped by 15% falling short of a demand of 69,143 units across eight major cities during January-March 2024, according to Industry experts. Only Bengaluru and Mumbai saw a rise in new housing supply, while other major cities like Delhi-NCR and Chennai experienced a decline. This quarter’s high-end and luxury segment accounted for 34% of total residential property launches. Additionally, listed, large, and regionally reputed developers contributed over 38% to the overall launches.

According to industry sources, the new supply of housing properties decreased to 69,143 units during January-March 2024 from 81,167 units in the same period last year. Among cities, Bengaluru saw an increase in new supply to 8,848 units from 7,777 units. The new supply marginally increased to 19,461 units in the Mumbai region from 19,063 units.

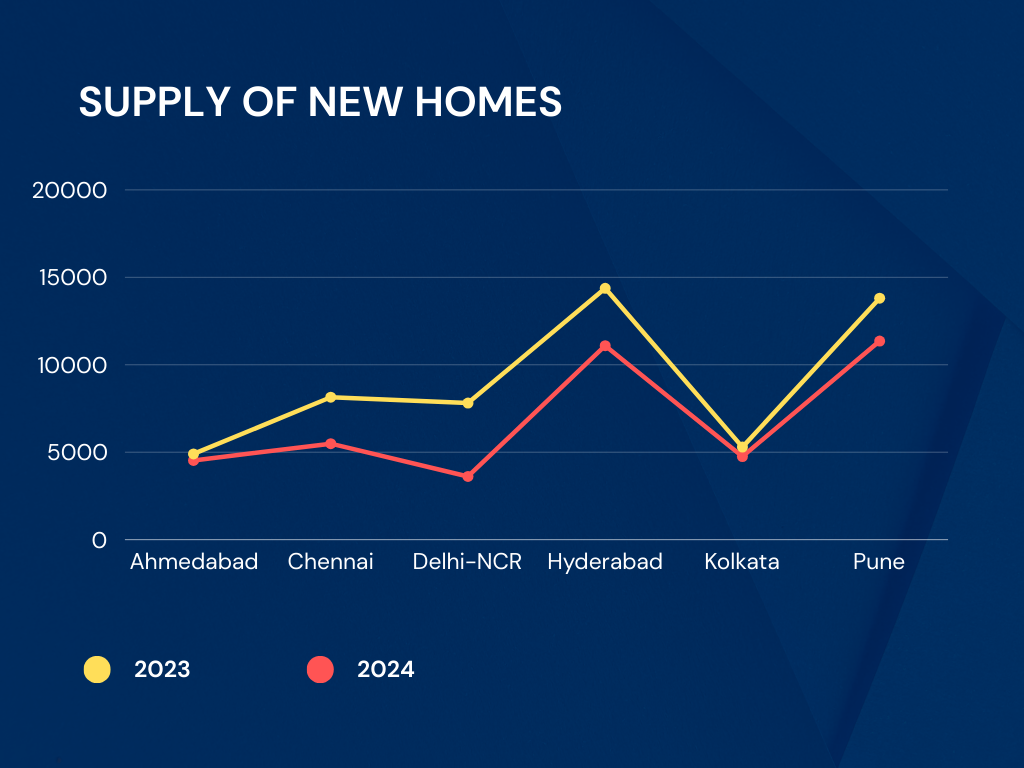

In 2023-24, Gujarat and Ahmedabad experienced a decrease in new affordable housing projects as consumer preferences shifted towards larger homes, impacting property prices. Additionally, the absence of tax benefits affected the launch of new projects. The new supply of homes in Ahmedabad fell to 4,529 units from 4,901 units. Chennai witnessed a decline in launches to 5,490 units from 8,144 units.

New supply in Delhi-NCR plunged to 3,614 units from 7,813 units. Hyderabad saw a decrease to 11,090 units from 14,371 units, while Kolkata witnessed a decline to 4,753 units from 5,292 units. The new supply of residential properties in Pune decreased to 11,358 units during January-March 2024 from 13,806 units in the corresponding period of the previous year. Another crucial factor is obtaining development approvals from the designated statutory authority. Under the RERA regime, developers are required to have all necessary approvals before launching a project. The time needed to secure these pre-development approvals ranges from six to twelve months, depending on the city.

Impact on the Real Estate Market

While new project launches may have experienced a slight dip recently, this is likely a temporary blip. Unsold inventory across major cities saw a minimal increase of just 1% every quarter. The bigger picture remains positive: overall market dynamics and buyer sentiment are strong, driven by increased demand in previous quarters. This trend is expected to continue, encouraging developers to launch more projects.

A temporary slowdown in new launches can be partially attributed to developers adopting a wait-and-see approach during the current election season. However, this doesn’t reflect a lack of confidence. Land deals tell a different story – developers have been actively acquiring land, particularly for residential projects. Land acquired in 2023 alone surpassed 2,700 acres; a staggering 125% increase compared to 2021. Market trends foresee this land buying spree suggests a strong pipeline of future projects once the elections are over.

U