No matter the situation in the global economy, the real estate market in India has been a lucrative investment option for Non-Resident Indians (NRIs). Indian real estate has been the fall-back option in troubled times. The bulwark that can weather all storms.

India’s central bank (RBI) allows NRIs to freely purchase immovable property, including residential and commercial assets. For dollar-heavy NRIs, the Indian realty market has offered consistent returns on investments.

But are NRIs eligible for home loans in India? What are their funding options for buying a property? Can they avail tax benefits on a home loan? We spoke to our finance expert and got some of the most commonly asked questions answered.

Here are the excerpts.

Can NRIs avail a home loan from Indian banks?

Yes. NRIs can avail home loans from any bank approved by the National Housing Bank (NHB). There are a few non-banking financial companies (NBFCs) also that offer home loans to NRIs.

What about the interest rates?

The interest rate on a home loan for NRIs is same as for citizens residing in India.

What about the mode of payment?

For buying a property in India, the money should come through banking channels only. NRIs can pay instalments, interest, and other charges via remittances from outside India through their non-resident external (NRE) rupee or non-resident ordinary (NRO) or foreign currency non-resident (FCNR) account, maintained in India. Post-dated cheques can also be issued.

The payment cannot be made in the form of traveller’s cheques or foreign currency.

What about the eligibility criteria?

There are a few variations when it comes to the eligibility criteria for home loans for NRIs. However, these things vary from bank to bank.

● Salary criteria: For NRIs, there is a minimum salary criterion. For instance, those working in any of the Gulf Cooperation Council (GCC) countries should have a minimum monthly income of 5,000AED (United Arab Emirates Dirham). For those working in the US, the minimum monthly salary should be $3,000.

● If you are self-employed, then you must have stayed abroad for a minimum of three years.

● Professional and educational qualifications also play a significant role. NRIs applying for home loans should be at least graduates.

What is the loan-to-value ratio for NRIs?

As per RBI norms, the bank can fund a maximum of 80% of the total value of the property. The remaining 20% should come from the borrower.

What is the loan tenure?

Well, this varies from bank to bank. For instance, HDFC offers up to 20-30 years while for other banks it is 10-15 years.

Is there any other option for funding?

If you are still settled abroad and have income accruing there, you can use that for funding your property purchase.

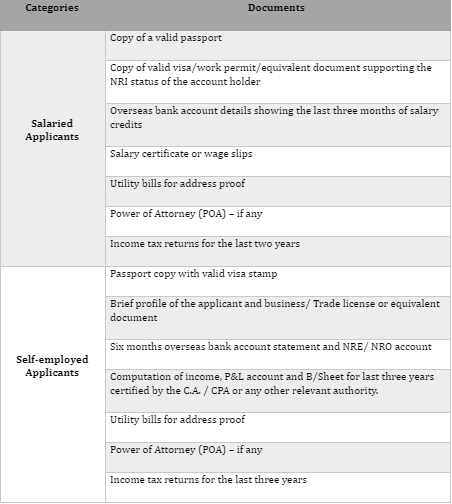

What are the essential documents required for a home loan?

- Passport and visa

- PIO/OCI Card

- Appointment letter’s copy and contract from the company employing the applicant

- The labour card/identity card

- Bank statements for the last six months

List of classified documents for salaried and self-employed non-resident applicants

What if the PIO card is not available?

If you do not have a Persons of Indian Origin (PIO) card, you can use photocopies of any of the following documents:

✓ The current passport, with birthplace as India

✓ The Indian passport, if held by the individual earlier

✓ Parents/grandparents Indian passport/birth certificate/marriage certificate substantiating the individuals claim as a person of Indian origin

Can NRIs avail tax benefits on a home loan?

There are no tax benefits for NRI customers taking a home loan unless they file returns and become eligible for tax rebates.

If the salary earned abroad is the only source of income, then you cannot claim tax exemption on home loan repayment since it is not taxable in India.

However, you can benefit from the tax deductions if you have some income that is taxable in India. In that case, you can claim deductions on the repayment of interest and principal from taxable income as per Section 24, 80C, and 80EE of the Income Tax Act.

Still got some doubts? Feel free to ask your questions in the comments below. Now you can also send your questions to us on Quora.

Hello NIKUNJ JOSHI Your post gave me a lot of help to know that how to get home loans in India, so keep posting in the future like this. You can write about this topic of NRI home loans in India.