Planning to spruce up your home but are worried about the finances? We have a simple suggestion. Consider home improvement loans. Wondering what a home improvement loan is?

Well, it is a loan offered for renovating or remodelling a house. You can avail it for remodelling, painting, internal and external repairs, or even bigger construction work such as adding a floor.

Let’s take a deep dive into the nitty-gritty of the home improvement loan.

The eligibility criteria

While there may be variations from bank to bank, here are some basic eligibility guidelines.

- You can apply as an individual or jointly with the other owners of the house being the co-applicants.

- Both salaried and self-employed individuals can apply for a home improvement loan.

- The minimum age limit is 21 years of age. The maximum age is restricted to your retirement age.

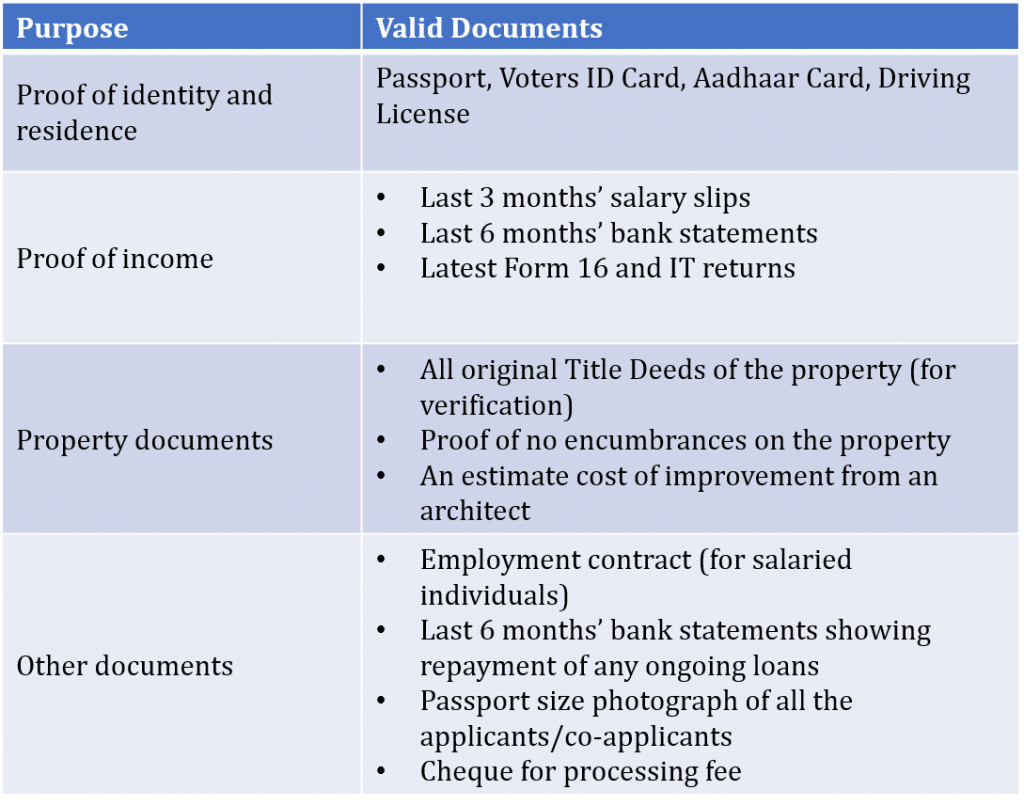

The documents you need

Like any other loan, the process of availing a home improvement loan will be much smoother if all the documents are in place. We have curated a list of documents that you must organise in a folder along with the photocopies.

Are there any tax benefits?

Yes.

Under Section 24(b) of the Income Tax Act, you can avail deductions of up to Rs 30,000 per annum for the interest paid. Both the owner and co-owners are eligible for tax deductions.

How to select the best lender?

We suggest choosing the same lender where you have an existing home loan (if any) for a smoother process. This is the faster way of getting a loan approved as the bank already has your documents.

However, in such a case, your property would act as collateral for this loan.

Opting for the same lender also comes with more benefits in terms of funds. Let’s take HDFC

example. An existing HDFC customer availing a home improvement loan of up to Rs 30 Lakh will get 100% of the improvement estimate. However, for a new customer availing the same amount, about 90% of the improvement estimate will be released.

The finer details

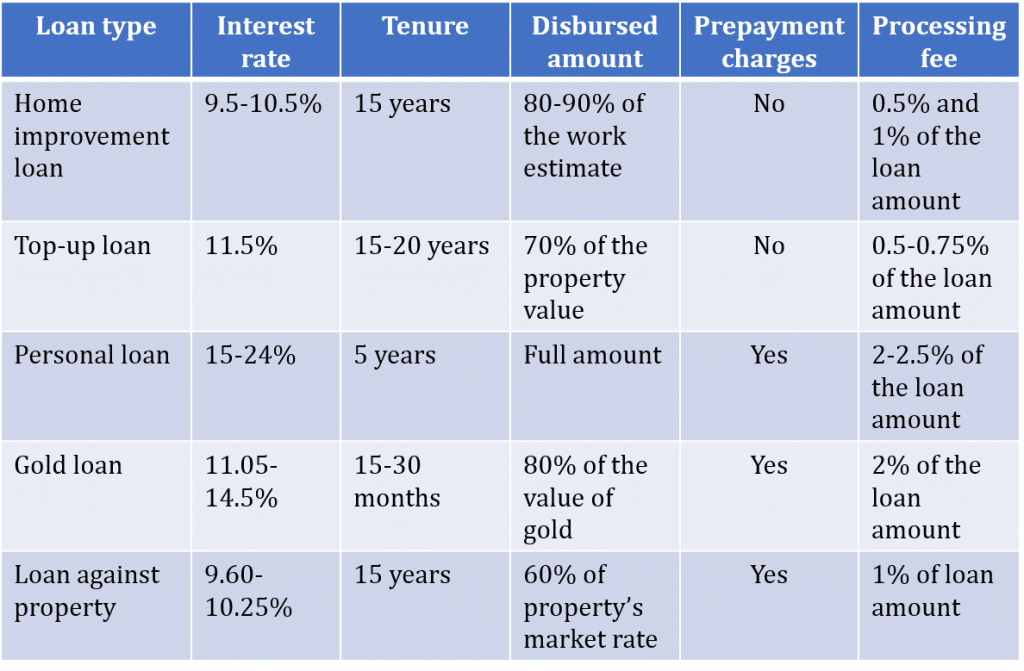

As with a regular home loan, the maximum tenure for a home improvement loan is 15 years. At present, the average interest rate is in the range of 9.5-10.5%, depending on the lender, loan amount, and eligibility.

The processing fee for these loans generally ranges between 0.5% and 1% of the loan amount.

Are there any alternatives?

While it is wise to go for a home improvement loan for any remodelling or renovation, there are a few more options that you can explore. These include:

Top-up loan: You can take this over and above your existing home loan. However, it can only be taken after a certain number of years of the home loan being sanctioned. For most banks, it is fixed at 3-6 years. The tenure is typically 15-20 years, depending on the tenure of the existing home loan.

The loan-to-value ratio for top-up loans is restricted to 70% of the property value. The processing fee is in the range of 0.5-0.75% of the loan amount.

You can also avail tax deductions if you are availing the top-up loan for home improvement.

Personal loan: You can also avail a personal loan for home renovation. However, the interest rates and prepayment charges for this is comparatively higher when compared to other available options. This is because no collateral is needed for a personal loan and the disbursal happens within two to three working days.

The maximum tenure offered is usually five years, which means that your EMIs would be higher compared to other loans.

Gold loan: Let’s assume you are not eligible for a home improvement loan. For example, the house is not in your name. In such situations, you can opt for a gold loan. This is similar to a personal loan with high-interest rates and faster disbursal.

With a gold loan, you get up to 80% of the value of gold for 12-15 months. This essentially means that you need to pledge more gold for higher amounts and pay higher EMIs.

Loan against property: If your home loan is over, you could consider taking a loan against your property. It comes with better rates and longer tenures when compared to a personal loan. However, in this case, you will only get 50-60% of the property’s market value.

RoofandFloor verdict

After analysing all the factors mentioned above, we believe that a home improvement loan might be the best option, followed by a top-up loan. What do you think?

(Note: The interest rates, tenure, and prepayment charges may vary from bank to bank).

You can also use your Provident Fund for this. All said and done, it is always better to save for home renovation rather than opting for a loan.

The good and informative article it is. I really appreciate your work.

God bless you.

Thanks.