“Is it mandatory to take insurance on the home loan?” asked Abhinav Kumar, one of our followers on Facebook. During his home loan application, the bank personnel told him that he had to buy an insurance policy, as per the Reserve Bank of India’s (RBI) guidelines. Is it true? Well, not really, Abhinav!

Opting for an insurance policy on a home loan is entirely the borrower’s prerogative.

If your bank is forcing you to buy one from them, it may be because they are receiving a commission from a particular insurance company.

Let’s explore further.

The home loan insurance covers a borrower’s outstanding loan liability. It is useful in case of unfortunate events like loss of income or death of the person paying the EMIs. In such scenarios, the insurance company will settle the remaining dues with the bank.

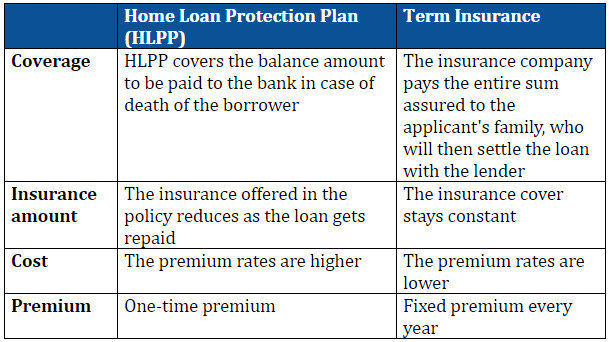

Difference between home loan protection plan and term insurance

The policy coverage

First thing first, this is an insurance for your home loan and not your home. Thus, just your home loan is secured. You will still have to get your home insured.

(Read More: Why Home Insurance Is a Necessity, Not a Luxury)

Like your car or home insurance, you will have to pay a premium for this as well. The premium depends on:

- Your age: The older you are, the higher the premium

- Tenure: The longer the tenure, the higher the premium

- Loan amount: Premium is higher for a huge loan amount

- Interestingly, if your medical history is sound, you will pay a lower premium. A compelling reason to hit the gym?

Know the tax implications

If you pay the premium yourself, you can claim tax deduction under Section 80C of the Income Tax Act. But if your lender pays the insurance premium (which means it is a part of your loan), then you cannot claim any deductions.

When does this policy lapse?

It can lapse in the following scenarios:

- Upon full repayment of the loan

- The demise of the borrower

- Transfer of the loan to another bank

What if the bank refuses to sanction your loan?

Trust us, there is nothing to worry about. Just follow our step-by-step guide and you will be sorted.

Step 1: Do not succumb

We are sure that after reading our post, you are clear about the RBI guidelines. Communicate this to your bank that you are aware of the rules and will take necessary actions if needed.

Step 2: Make your case stronger

Ask the bank to give it in writing that it is mandatory to take home loan insurance. Tell them that you would like to inquire more about this with the banking ombudsman. Don’t worry if you don’t know who the banking ombudsman is. He is just an official appointed to investigate people’s complaints against a company or an organisation.

Step 3: Stay calm and reject the offer

The thumb rule is not to look desperate while availing a home loan service. Just reject the offer and the bank will surely come back to you.

Have you come across a situation like this? We would love to know your experiences in the comments.

The million-dollar question: Should you buy a home loan insurance policy?

If your pocket allows, you should consider it. From our car to home to bike, we get everything insured, then why not the home loan?

However, you need not take it from the same bank as you are taking a loan. Always weigh the pros and cons of different policies offered by different insurance companies. It is also advisable to consult a financial expert and figure out what works for you – the home loan protection plan or the term-insurance plan. Another way is to be financially sound while availing a home loan.

Just remember, smart buyers are informed buyers!

I have been looking out for a home loan . I completed entire process .at the very end when I was about to sign they informed about the insurance . The premium was hefty 2.9 Lacs and mandatory.

I rejected the offer as of now . Let’s see what happens