Planning to buy a plot of land for constructing your home? A brave decision! As per our home expert Swati, “You are about to embark on a journey and an experience that can be bittersweet while it lasts, filled with exciting as well as stress-filled moments.”

Building a home is a long-drawn process that requires you to be on your toes all the time. From hiring an architect to getting construction workers on board, you will have a lot to deal with. So, we thought of simplifying the finance aspect for you.

When you build a home, taking separate loans for land and construction may overburden your finances. Instead, you can apply for a composite loan, which covers both construction and land costs. Let’s delve deeper.

Understanding composite loan

Individuals who plan to buy a plot of land on loan and construct a home on the same can avail a composite loan. These loans are only for residential construction.

The loan-to-value ratio is slightly higher than a regular home loan and varies between 60-75%. So, make sure you have at least 35-40% of the total amount as down payment. When compared to a home loan, the interest rate is also slightly higher.

Prerequisites for composite loan

One of the prerequisites for this loan is to give your lender the guarantee that you will start construction within one year from the date of land purchase. Some others include:

- The estimated cost of construction is mandatory. This can be approximate.

- An architect or a chartered accountant must validate the estimated value.

- Lastly, the technical report is needed to evaluate the progress and level of construction.

The disbursement

Unlike a home loan, which gets credited to the builder’s account, the composite loan is credited to your personal account. It is disbursed in instalments called ‘tranches.’

The first tranche is disbursed when you buy land, and the rest are released at various stages of construction. Usually, the entire loan is disbursed in four to five tranches.

For the disbursal of each tranche, you need to submit the following documents:

- Demand letter

- A certificate from your architect stating the construction status

- Photographic evidence of each stage of completion

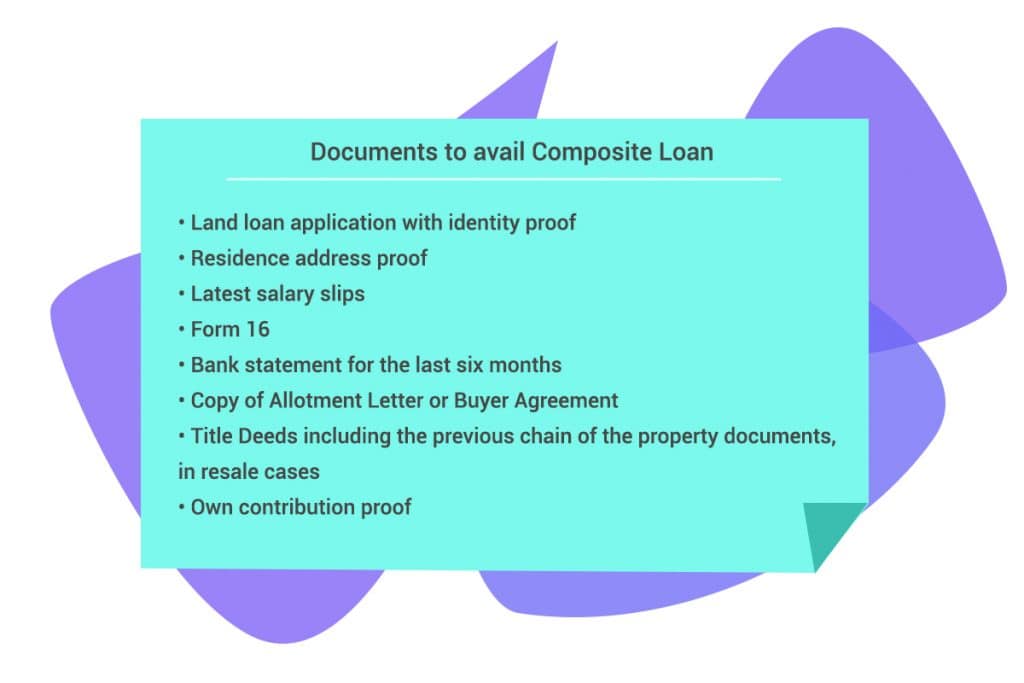

Documents to avail composite loan

For availing a composite loan, you need to submit the following documents.

Are there tax benefits?

Yes, but there are certain conditions. You must complete the construction within three years of buying the land. The tax deduction will be applicable in the last year under Section 80C.

Once the construction is complete, you have to get a completion certificate from the architect and submit it to your bank. From the year of completion, you can start taking tax benefits like a usual home loan.

In a composite loan, the onus of getting completion certificate rest with the borrower. Without this certificate, it is just considered as a land loan. After the submission of this important document, the loan gets converted to a regular home loan.

The closure

If your loan is on the floating interest rate, you don’t have to pay any prepayment charges. If you are on fixed interest rates, you will have to pay the requisite charges.

Closing words

A composite loan is a great option if you plan to start the construction immediately or within the stipulated timeline. If not, opting for land loan and construction loan separately would be better.

Hi Nikunj ,

What if i get a composite loan sactioned in April 2020 and complete the construction/completion of house by Feb 2021 … and from Apr 20 to Feb 2021 in 11 months i had paid total EMI of 3 lakhs out of which 2 lakhs was interest component and 1 lakh was principal .

So in FY 20/21 tax return , can i claim tax benefit of total 2 lakhs on account of interest paid on my loan … ?