Since early November when the Indian Government announced the demonetization of Rs 500 and Rs 1000 currency notes, there has been widespread apprehension amongst home buyers and other stakeholders in the real estate economy. We have received several queries regarding the impact of currency ban from the perspective of a potential home buyer as well as that of investors.

Hence, we have prepared this Cheat Sheet on Demonetization and its impact on Real Estate Sector in India.

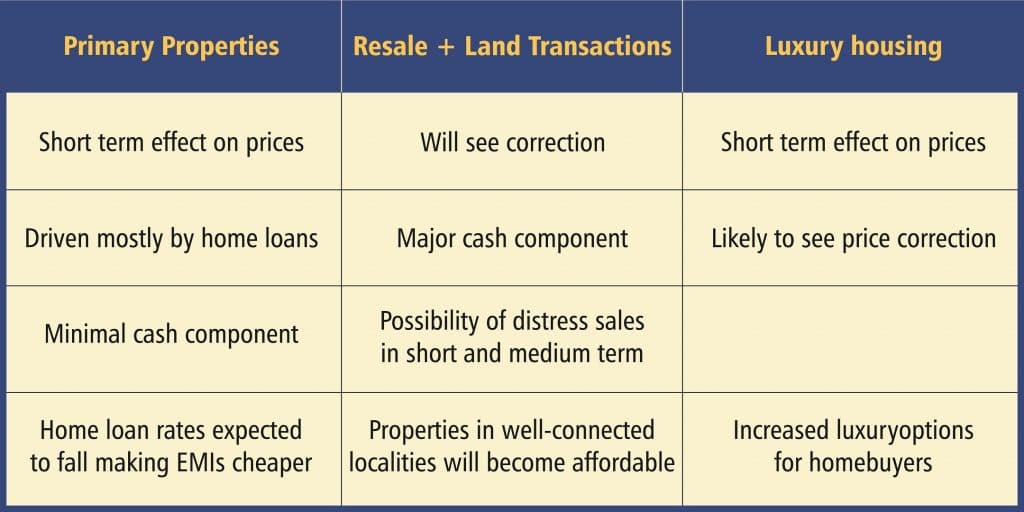

- Impact on Property Prices

- Primary Properties – In the short term, chances of prices coming down is low as this segment is driven mostly by home loans and has minimal cash component.

- Resale Properties – Resale and land transactions have always involved a major cash component and is expected to see correction. In the short and medium term, this segment is expected to see some distress sales.

- Luxury housing – In the short term, this is the segment that is very likely to see price correction.

Remember, these are all different segments and they can each behave in different ways, hence, keep that in mind while reading about market impact. But there is a prevailing negative sentiment about the industry and this will have an impact on prices for the next 6 months – discerning investors can turn this into an opportunity.

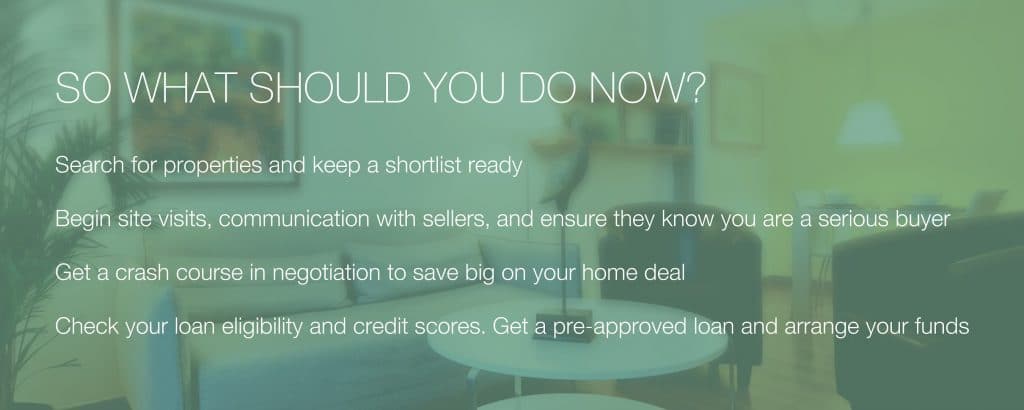

- Opportunity to save big on home deals

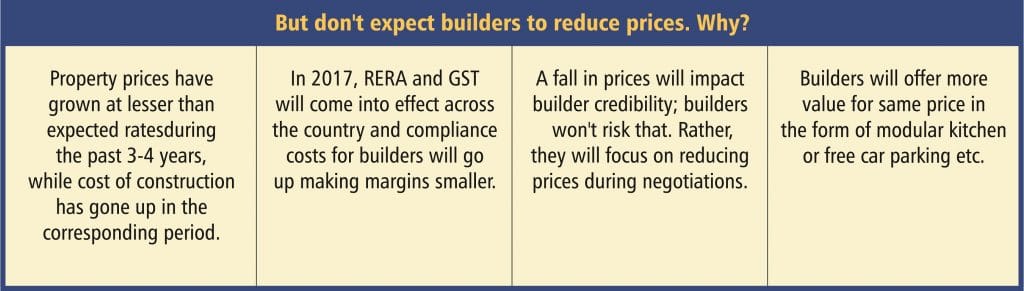

There is a perceived negativity and uncertainty in the market and this is expected to lower demand. Consequently, a fall in sales will affect the liquidity of builders who will, in turn, introduce attractive offers and other benefits to bring in buyers and prop up sales volumes. Remember, do not expect the builders to slash property prices. However, if you are a serious home buyer, your bargaining power with the builder has increased. They will be more willing to negotiate prices and there is increased possibility of builders offering more value for the same price in the form of modular kitchen or free car parking etc. The next six months promises to be a great opportunity to make big savings on buying homes.

- This is a good time to buy your first home. Why?

- Builders need cash liquidity to pay input costs for construction as well as wages. Builders will negotiate and offer best price possible to serious buyers.

- You have more options:

- Resale properties in well-connected localities that were out of budget will become affordable.

- Most first time home buyers use home finance/home loans. Home loan rates are expected to fall soon making EMIs go down making homes cheaper.

- You can get a bigger home at the same price.

- Resale, land could see distress sales

Resale and land segments have a huge cash component and demonetization has temporarily removed unaccounted for cash from the system. Buyers who could indulge in pay-cash-and-buy transactions are out for now and only those who use legal channels like finance/home loans are in play. This means, there is low demand for these segments and higher pressure on sellers to go for distress sales to maintain liquidity.

However, land prices will not directly have an impact on property prices. The distress sales that occur in this segment will not impact residential market as projects that come up here will not enter the market for at least another 4-5 years. Liquidity crunch will mean fewer new projects will be launched in the next 12-16 months.

The best time for a home buyer is the next 6 months. After that time, demand is expected to go up due to cheaper loans, newer currency will bring liquidity back into the system and create positive impact which will raise property prices. Additionally, there will be fewer new launches, raising demand for ready to occupy homes, which in turn will cause property prices to shoot north.

So best, the buyer’s market scenario will last for a maximum of 6 months.